Julian Howard, GAM’s Chief Multi-Asset Investment Strategist, outlines his latest multi-asset views, exploring how elevated market volatility, speculation around interest rates and geopolitical uncertainty are failing to reflect benign conditions in the world’s largest economy

09 October 2024

Review

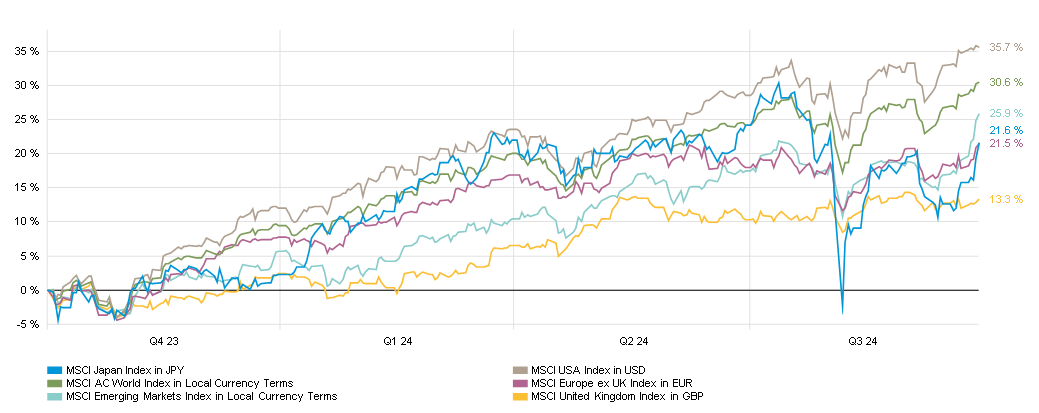

The MSCI AC World Index gained 5.0% in local currency terms during the third quarter of the year. On the surface this was a strong result and not far off the long-term annualised rate of return investors have come to expect from equities over the decades. But it did mask an episode of heightened volatility in late July to early August whose roots lay in three places. First of these was a sudden unwinding of technical positioning around the Japan carry trade in which traders borrowed in low-yielding Japanese yen to finance positions in higher-yielding currencies. The Bank of Japan (BoJ) arguably over-emphasised its desire to normalise interest rate policy and this led to a rapid reversal in positioning as market participants feared a sudden yen strengthening. Second was fears over the viability of the artificial intelligence (AI) revolution. While near-term profitability at the so-called AI ‘superscalers’ (supplying the enabling software and hardware) was probably not in doubt, some concerns were starting to be expressed about the slow take-up of AI across corporate America as well as potential bottlenecks in the huge energy supply required for data servers. Thirdly, there was the spectre of a potential slowdown in the US economy given that consumers were beginning to express caution in their spending habits. Together, this was enough to see the S&P 500 Index crater -8.8% from 16 July to 5 August, close to outright correction territory. Stock markets recovered however, perhaps reassured by the Bo’s extraordinary declaration that it would not raise interest rates at the risk of upsetting markets. Nvidia’s stellar results announcement helped too, as did better economic data and cooling inflation in the US, along with the increasing expectation of a 50 basis point (bps) cut in interest rates which was duly announced by the Federal Reserve following the mid-September policy meeting.

Elsewhere, late in the quarter China announced a significant stimulus package which boosted its beleaguered stock markets - and the wider MSCI Emerging Markets Index - in the hope that the economy might finally be turned around. In Europe, the very real prospect of stagnation resulted in the release of a seminal report by the eurozone’s top technocrat Mario Draghi proposing a raft of measures to stabilise and grow the economy in an increasingly uncertain world. In the meantime, the steady drumbeat of political and geopolitical uncertainty continued. No fewer than two assassination attempts on former President Donald Trump underscored the drama and division characterising this most fraught US election campaign, while the war in Ukraine saw a significant incursion into Russian territory even as Ukraine slowly but surely lost territory elsewhere. In the Middle East, outright war between Israel and Hezbollah in Lebanon looked all but inevitable. Amid all this, US equities dominated most other regions – yet again.

Chart 1: Emerging markets start to catch up but the last 12 months are America’s:

Performance from 30 Sep 2023 to 27 Sep 2024

Past performance is not an indicator of future performance and current or future trends.

Source: MSCI, Bloomberg, Policyuncertainty.com.

The views are those of the manager and are subject to change. For illustrative purposes only. Indices cannot be purchased and invested in directly. Please refer to Appendix for full explanation of indices shown.

Source: MSCI, Bloomberg, Policyuncertainty.com.

The views are those of the manager and are subject to change. For illustrative purposes only. Indices cannot be purchased and invested in directly. Please refer to Appendix for full explanation of indices shown.

Positioning

We did not change our investment views significantly during the third quarter, and sought to continue to take advantage of the superior real returns that stocks can offer over time, with intervening volatility addressed by sensible diversifying allocations sized according to each strategy’s risk/return objectives. We remained broadly engaged in equities, with an emphasis on US stocks in particular. This stems from the relative strength of the US economy as well as the US markets’ repeatedly demonstrated advantage in return on equity, innovation and management quality. Since we cannot by definition favour all regions, our bias towards the US position is offset by more neutral views on emerging markets (EM) and Japan as well as more cautious approaches to Europe and the UK. While EM including China offer a compelling structural story - and now a significant stimulus package - the latter faces particularly acute challenges which we feel require a more profound change of approach by the authorities. China therefore offers both upside but also persistent downside risks which makes us cautious around both it as a market and the wider EM index of which it is such a large constituent part.

For Europe and the UK, restoring medium-to-long-term growth presents a similarly momentous task requiring the kind of political consensus that has been notably absent in recent years. Away from stocks, our capital preservation approach rests primarily on fixed income markets. Our favoured areas include short-dated bond and money market instruments which still offer super risk-adjusted yield characteristics since central banks in the US, eurozone and UK have only just embarked on monetary policy loosening. We also see some appeal in traditional longer-dated government bonds for portfolio crash protection. Beyond these core fixed income areas, we also see the appeal of selected alternative investments. We have two areas of interest here: long/short merger arbitrage can potentially generate steady, modest returns from the flow of corporate M&A, while macro investing aims to capitalise on significant moves in interest rates and currencies.

Outlook

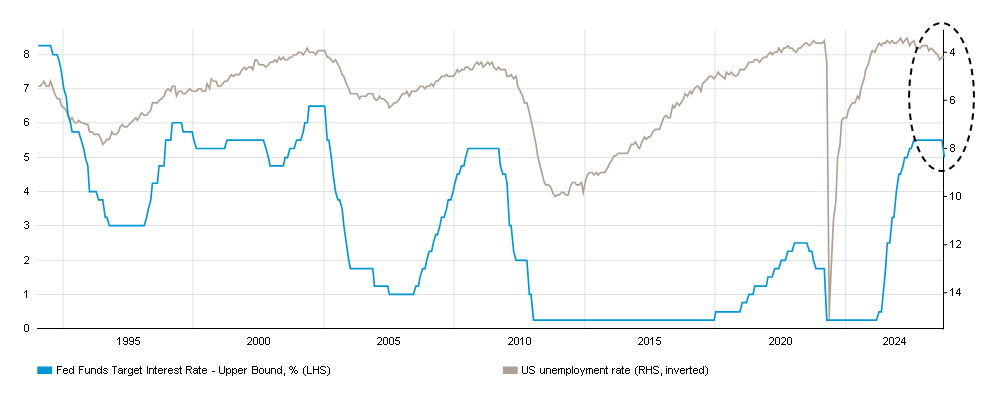

For many commentators, the only question that seems to matter today is whether the US can pull off the vaunted soft landing, ie in which inflation eases to normal levels without the economy falling into recession. Our sense is that this is very possible. Even if US headline inflation stabilises around its current 2.5% rate, the evidence is that the economy should continue to thrive. Usually the epicentre of any recession claims due to its close link with consumer behaviour, the employment picture today is attractive. Unemployment at 4.2% remains relatively low by historic standards, labour market participation is rising and job openings are still in good shape, all of which speaks of a growing job market. Consumers may be a little more cautious but retail sales are stable and sentiment has been rising for more than two years now according to the respected Michigan survey. All of which leads to the question of what effect will lower interest rates have, if any, on the US economy? Intriguingly, many US mortgage borrowers are enjoying long-term fixed rates locked in before rate rises began in earnest in 2022. And the economy itself seems less structurally exposed to the vagaries of interest rate policy than before – manufacturing and housebuilding are smaller sectors than they were twenty years ago, for example. Furthermore, cash-generative technology firms that make up an increasing share of the corporate landscape are less capital-intensive than their predecessors. If anything, interest rates being cut into an already-fair economy risks an unwanted inflationary surge as demand potentially lifts even higher. And lower rates will eventually mean lower yields for the holders of the whopping USD 6.3 trillion the Investment Company Institute estimates are currently parked in US money market accounts. But these risks seem unlikely to threaten the fundamentally sound US economy.

Away from the US, it is generally harder to be universally confident of benign outcomes. We will watch the progress of China’s stimulus package with interest but note that unless state-directed enterprise and economic management is moderated, unintended excesses will continue to haunt the Chinese economy. As for Europe and the UK, the challenges have been identified but addressing them requires a degree of unity and long-term planning that have eluded both respectively. Japan meanwhile looks set to continue struggling with balancing the need for monetary policy normalisation, ie higher interest rates, with its mighty export sector and the stock market’s addiction to a weak currency. Predictions around political and geopolitical volatility are by nature challenging. The wars in Ukraine and the Middle East are likely to drag on, particularly if proxies become more enmeshed on both sides. But investors can at least take some comfort from the fact that the US election will soon be over and that alone will remove an element of uncertainty from the scene. A deep irony underpins the election campaign, in that for all its savagery the two sides’ economic policies are not vastly different when it comes to the budget deficit and protectionism. Either way, with one last quarter to go, 2024 is shaping up to be another American year.

Chart 2: Are rate cuts even needed right now?

From 31 Dec 1989 to 27 Sep 2024

Past performance is not an indicator of future performance and current or future trends.

Source: Bloomberg

Source: Bloomberg

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The MSCI AC World Index is a stock index that captures large and mid-cap representation across 23 Developed Markets (DM) and 24 Emerging Markets (EM) countries. With 2,921 constituents, the index covers approximately 85% of the global investable equity opportunity set. The S&P 500 Index is a stock index tracking 500 of the largest, publicly traded companies in the United States.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in indices which do not reflect the deduction of the investment manager’s fees or other trading expenses. Such indices are provided for illustrative purposes only. Indices are unmanaged and do not incur management fees, transaction costs or other expenses associated with an investment strategy. Therefore, comparisons to indices have limitations. There can be no assurance that a portfolio will match or outperform any particular index or benchmark.

This article contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

This disclosure shall in no way constitute a waiver or limitation of any rights a person may have under such laws and/or regulations.

In the United Kingdom, this material has been issued and approved by GAM London Ltd, 8 Finsbury Circus, London EC2M 7GB, authorised and regulated by the Financial Conduct Authority.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The MSCI AC World Index is a stock index that captures large and mid-cap representation across 23 Developed Markets (DM) and 24 Emerging Markets (EM) countries. With 2,921 constituents, the index covers approximately 85% of the global investable equity opportunity set. The S&P 500 Index is a stock index tracking 500 of the largest, publicly traded companies in the United States.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in indices which do not reflect the deduction of the investment manager’s fees or other trading expenses. Such indices are provided for illustrative purposes only. Indices are unmanaged and do not incur management fees, transaction costs or other expenses associated with an investment strategy. Therefore, comparisons to indices have limitations. There can be no assurance that a portfolio will match or outperform any particular index or benchmark.

This article contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

This disclosure shall in no way constitute a waiver or limitation of any rights a person may have under such laws and/or regulations.

In the United Kingdom, this material has been issued and approved by GAM London Ltd, 8 Finsbury Circus, London EC2M 7GB, authorised and regulated by the Financial Conduct Authority.