More than ever before, Asia Pacific producers are key players in the global clean energy revolution. But with geopolitical tensions rising and the threat of disruption looming ever larger, GAM Investments’ Meera Patel explores factors behind the risks and opportunities for investors in a region harnessing the might of the green economy to bolster its long-term economic prospects.

22 July 2024

Over the past decade, we have witnessed the emergence of a growing sustainability community in Asia Pacific spanning governments, corporates and investors. This is primarily due to the region’s significant role from an economic, demographic and emissions perspective, but also a growing necessity as the impacts of climate change are experienced firsthand.

Green economy supply chains are now more reliant on Asian production than ever, with China dominating solar panel, critical mineral processing and battery production, while Japan and South Korea lead on green hydrogen strategy and commercialisation driving regional trade agreements.

Amid rising geopolitical tensions and a continuing wave of election surprises, major Asian economies using the green economy as a driver to boost future growth and enhance energy security are exposed to the uncertainty around global regulatory repeals creating both tailwinds and headwinds.

Why does this matter?

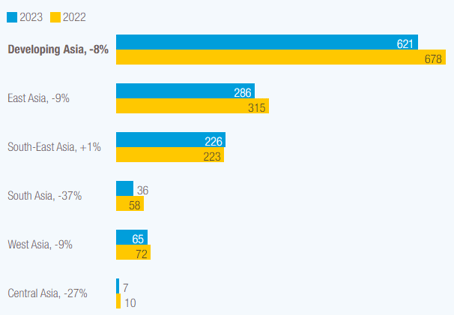

Since the US signed its mighty USD 370 billion Inflation Reduction Act (IRA) into law in August 20221, Asia’s clean energy supply chains and Foreign Direct Investment (FDI) levels have been negatively impacted, with the UN Trade and Development’s 2024 World Investment Report estimating an 8% decrease in FDI in developing Asia during 20232.

Aimed at lowering energy costs for US households and businesses by accelerating private investment in clean energy solutions, strengthening local supply chains and creating local employment opportunities, the IRA has redirected investment flows amid a challenging high interest rate environment and oversupply dilemma for clean energy stocks.

Foreign direct investment (FDI) by region, billions of dollars, per cent, 2022-2023

Source: UN Trade and Development (UNTAD)

A Republican sweep in November’s US Presidential elections could potentially weaken the rollout and implementation of the IRA, with consumer-facing incentives such as electric vehicle (EV) tax credits and highly technology-dependent sectors such as hydrogen and carbon capture facing the most pressure. It is also likely that a renewed focus on foreign entity concerns will dominate headlines, negatively impacting Chinese EV and clean energy sectors.

What is the opportunity from an investment perspective?

Republican-controlled states have received the majority of benefits from an IRA-driven manufacturing revival and associated job creation, so it is highly unlikely that all support will be repealed regardless of which party wins in November. Given the challenges behind aging infrastructure, utility-scale solar and energy storage manufacturing will remain key strategic priorities and have dominated new facilities announcements to date. Several Korean clean energy companies in this space are well positioned to benefit from continued support and provide the added integration benefit of operating across all key solar supply chains while investing in leading battery coating technology which could lower costs by 17%-30%.3

Source: American Clean Power (cleanpower.org)

Source: NPR

Asia accounts for over two thirds of global heavy industry capacity, and it is currently widely accepted that the only way to get these industries to net zero at the required scale is via three advanced technologies: electric arc furnaces, hydrogen and carbon capture. Although a number of decarbonisation project proposals have been announced by leading industrial companies, energy inefficiencies and cost remain primary inhibitors to scaling up these technologies. However, on a relative basis, Asia has made significant progress. For example, this is evident by China’s ability to produce hydrogen at approximately half the cost of European equivalents, enabling scalability of electrolysers and the knock-on impact of rapid cost deflation as seen with other parts of the clean energy value chain. Any IRA-related repeals on hydrogen and carbon capture could provide an added tailwind to Asian companies.

Source: BNEF

There is one legacy energy source most countries and policymakers seem to agree on as being critical to meeting net zero targets: nuclear’s role in the energy mix. Although the transition from coal and gas-fired facilities to atomic plants is well underway, engineering challenges remain an issue. In the short term, the US ban on imported uranium products from Russia, which accounts for 40% of global capacity4, could tighten supplies with two leading European-based uranium enrichment companies set to benefit from this disruption. In Asia, as part of the Sapporo 5 partnership, Japan has committed to increase their enrichment from 75 tons to 450 tons per year by 20275, while China has spent the last two decades becoming increasingly self-sufficient in this area.

Although geopolitical dynamics remain unpredictable, understanding the impact of various scenarios is key to identifying risks, inflationary pressures and both the progress or derailing of ambitious net zero goals.

1 International Energy Agency, November 2023: www.iea.org/policies/16156-inflation-reduction-act-of-2022

2UNCTAD: https://unctad.org/publication/world-investment-report-2024

3Bloomberg

4Bellona: https://bellona.org/news/nuclear-issues/2024-05-how-will-the-us-ban-russian-enriched-uranium-impact-both-countries

5US Department of Energy: https://www.energy.gov/ne/articles/sapporo-5-leaders-make-significant-progress-securing-reliable-nuclear-fuel-supply-chain

2UNCTAD: https://unctad.org/publication/world-investment-report-2024

3Bloomberg

4Bellona: https://bellona.org/news/nuclear-issues/2024-05-how-will-the-us-ban-russian-enriched-uranium-impact-both-countries

5US Department of Energy: https://www.energy.gov/ne/articles/sapporo-5-leaders-make-significant-progress-securing-reliable-nuclear-fuel-supply-chain

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. This disclosure shall in no way constitute a waiver or limitation of any rights a person may have under such laws and/or regulations.

In the United Kingdom, this material has been issued and approved by GAM London Ltd, 8 Finsbury Circus, London EC2M 7GB, authorised and regulated by the Financial Conduct Authority.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. This disclosure shall in no way constitute a waiver or limitation of any rights a person may have under such laws and/or regulations.

In the United Kingdom, this material has been issued and approved by GAM London Ltd, 8 Finsbury Circus, London EC2M 7GB, authorised and regulated by the Financial Conduct Authority.