The Trump administration’s attempt to shake up the global trade order has triggered extreme volatility across global markets. While compressed credit spreads appear to offer limited scope for attractive returns, Tom Mansley explains his view that a “sweet spot” in US mature mortgage-backed assets offers a compelling proposition for investors.

11 July 2025

Policy uncertainty has triggered volatile start to Trump 2.0

The Trump administration’s unconventional policy approach – from the imposition of sweeping trade tariffs, deep cuts to government budgets and plans for large corporate tax cuts and deregulation – has created unprecedented levels of uncertainty for investors.

While the losses suffered in the aftermath of 2 April “Liberation Day” have been recouped, the whole episode has not come without cost.

Treasury yields have risen, the US dollar has slumped, and gold, a conventional haven in times of uncertainty, has soared, raising questions as to whether the US currency still holds the same ‘safe haven’ appeal.

Trump tariff is not impacting US housing

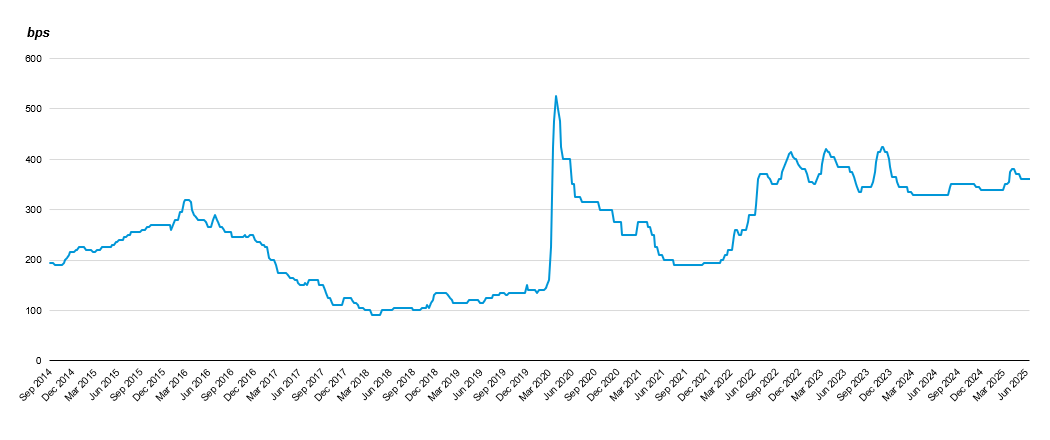

While uncertainty over US policy on trade and immigration, as well as the proposed budget bill that could significantly increase government debt levels – has impacted on Treasuries and the US dollar, swiftly changing US government policies have not targeted domestic consumers, or the housing sector. In our view, the Residential Mortgage-Backed Securities (RMBS) space’s status as a relative haven remains unrecognised and underappreciated by investors, with wide spreads, both historically and relative to asset classes such as high yield bonds.

Legacy RMBS Spreads

Non-Agency

Past and current trends should not be relied upon as an indicator of future trends.

Source: TRACE, Wells Fargo Securities, June 20, 2025. Chart updated on quarterly basis. For illustrative purposes only.

Source: TRACE, Wells Fargo Securities, June 20, 2025. Chart updated on quarterly basis. For illustrative purposes only.

Safe as houses? Why we are positive on the outlook for the US residential sector

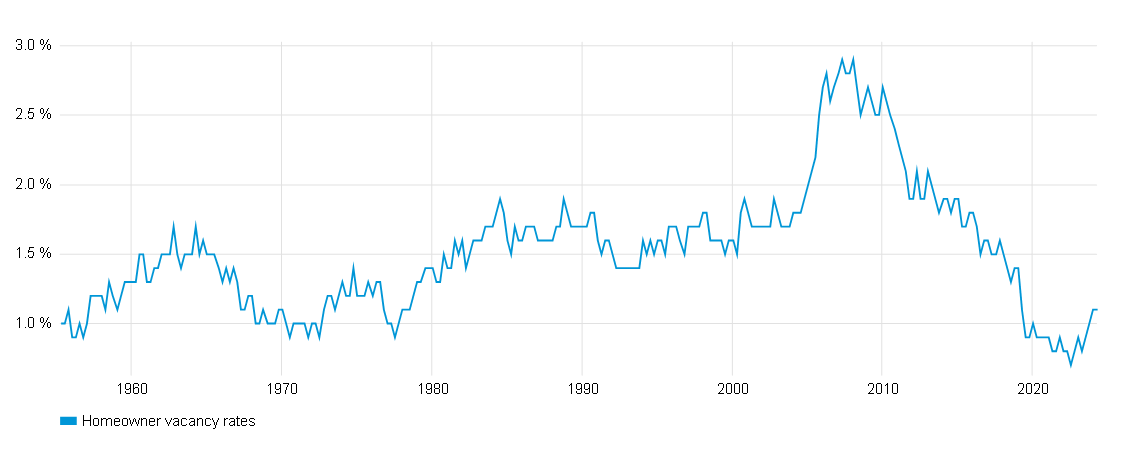

Despite volatility in the wider bond and equity markets, we believe the story of the housing market is one of relative consistency and underlying strength. Driven by steady demand from buyers, low supply, and positive lending patterns, the overriding theme we associate with residential property assets is stability. Reflecting the positive economic backdrop, homeowner vacancy rates of around one percent are close to their multi-decade historical lows.

Homeowner vacancy rates in the U.S.

From 31 March 1956 to 31 March 2025

Past performance is not an indicator of future performance and current or future trends.

Source: Bloomberg.

Source: Bloomberg.

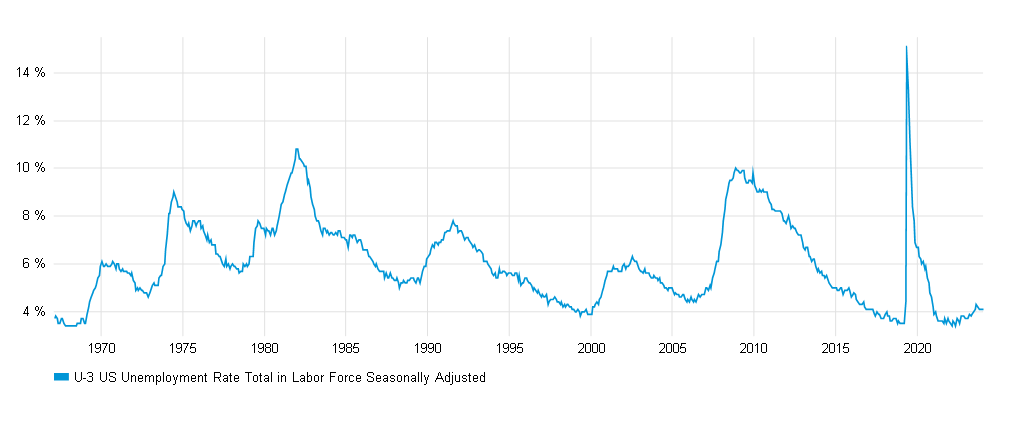

Underpinned by the resilience of the job market – which manifests in low unemployment and rising wages – default rates and foreclosures remain extremely low, reflecting the robust credit status of borrowers, and the priority they are putting on servicing their mortgage payments.

US Unemployment Rate

From 31 January 1968 to 31 December 2024

Source: Bloomberg.

Targeting the ‘sweetest spot’ in the vast US mortgage-backed securities universe

The sheer scale of the mortgage-backed securities universe comes as a surprise to some investors – a highly liquid, diversified market in excess of USD 10.8 trillion1, accounting for approximately one quarter of the entire US fixed income universe. As a very large segment of the US fixed income market, the RMBS space provides active managers with immense opportunities to be highly selective.

While some investors may favour agency loans, we instead favour core holdings of more mature, seasoned residential mortgages, especially those issued around the 2004-2008 period. We believe multiple factors combine to make these assets particularly attractive:

- High underlying asset value relative to the loan size: These vintage mortgages were issued when home prices were appreciably lower than today, meaning borrowers have since accrued very significant equity in their properties. This means that as secured lenders, investors in these assets benefit from the reassurance of a very high asset value with a comparatively low loan value.

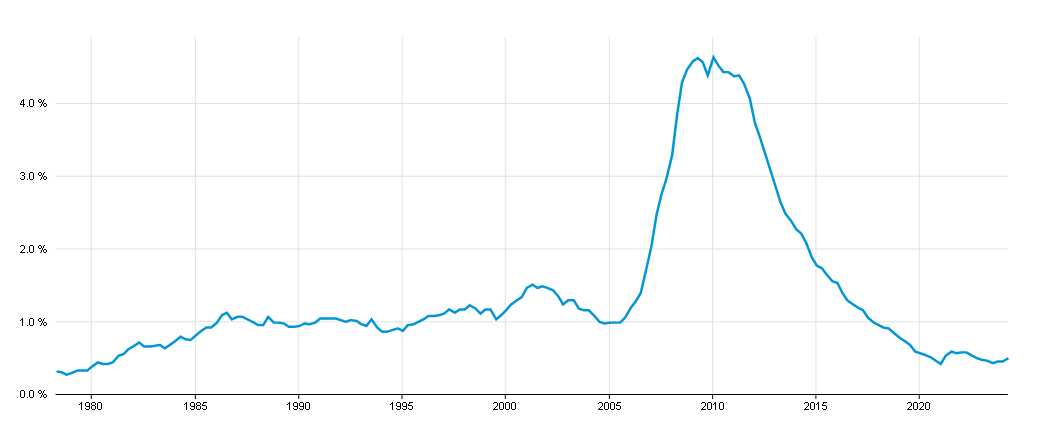

- Seasoned mortgagees have a stable history of repayments: In our view, the peak default risk for mortgages originated around the 2005 ‘sweet spot’ was in the aftermath of the 2007-2008 Global Financial Crisis (GFC). Since then, foreclosure rates have tumbled below even their 1990-2005 base, suggesting mortgage holders have serviced their debts through bad times and good, while also capitalising on the sustained climb in property values.

Foreclosures as % of total loans NSA

From 31 March 1979 to 31 March 2025

Past performance is not an indicator of future performance and current or future trends.

Past performance is not an indicator of future performance and current or future trends.

Source: Bloomberg. - Borrowers have shown low sensitivity to interest rate swings: Borrowers that have mortgages originated in 2004-2008 that re still outstanding today resisted any temptation to refinance even when rates were as low as 3%. We believe that with refinancing rates now closer to 7%2, they are now highly unlikely to prepay their loans, and will instead typically continue regular payments. As many older mortgages are now discount bonds (ie trading below par), even if mortgagees did elect to repay faster, RMBS investors would essentially get their capital back rapidly from a discount bond that goes to par faster, a move that also boosts their yield ., So any borrowers deciding to repay faster effectively help to support the income element of the total returns investors receive from RMBS portfolios.

Hedging interest rate risk to harvest a premium

Holding a core portfolio of seasoned, stable mortgages, especially one modelled to target borrowers repaying over the full course of their term, should, in our view, help to reduce prepayment risk and thereby make duration more predictable. However, interest rate risk remains, but that can be readily mitigated through the use of Treasury bond futures, which we use to reduce the interest rate risk of the portfolio and further lower the volatility. By so doing, we believe that a portfolio can replicate the income of high yield bond assets, while adding the benefit of low correlation to other asset classes.

RMBS – built on stronger foundations

While shockwaves from global events such as the 1998 Long Term Capital Management failure, the 2007-08 GFC and the Covid pandemic can impact on virtually any asset class, we believe that the US mortgage bond market is now better insulated than ever by a range of supportive domestic factors, such as the excess of demand over supply for houses, and the robust employment market. Moreover, beyond the US government policy-related uncertainties which continue to overshadow many risk-based assets, particularly in areas such as manufacturing reliant on cross-border trade, energy or pharmaceuticals, we believe that areas like housing and consumer credit will remain off the government political agenda, thereby reducing the risk of adverse regulatory developments.

In the present environment of policy-driven uncertainty, we believe that RMBS portfolios, especially those concentrating on seasoned mortgages, can continue to deliver attractive returns for investors. In our view, in a volatile investment environment, these returns could have even more appeal. While these 2004-2008 originated bonds will, by the very nature of term-based mortgages, not be available in perpetuity, we believe that this is an excellent entry point to purchase these assets that should continue to represent a highly attractive risk versus reward proposition for investors over the coming years.

While other equally attractive opportunities may emerge in the vast RMBS space over time, in our view, investors could do well to capitalise on these underappreciated assets while they are still available.

Tom Mansley leads the mortgage-backed securities strategy at GAM Investments.

1Source: Securities Industry and Financial Markets Association (SIFMA), December 2021

2Source: Bloomberg, July 2025

2Source: Bloomberg, July 2025