Julian Howard, GAM’s Chief Multi-Asset Investment Strategist, outlines his latest multi-asset views, exploring how an almost unprecedented period of turmoil has been greeted by relative calm in global stockmarkets. However, a lack of consensus across asset classes points to opportunities and risks for investors looking for diversification.

09 July 2025

Review

The MSCI AC World Index delivered an exceptionally strong performance in the second quarter of 2025, posting a 9.5%* return in local currency terms. This was little short of extraordinary given the geopolitical turmoil unleashed on global investors. The second quarter was barely days old when the Trump administration heralded Liberation Day in which blanket tariffs were applied on imports from all of the US’s trading partners, with the threat of more unless they negotiated. Stockmarkets around the world promptly dived, with commentators and strategists breathlessly declaring the end of the world trading order as they knew it.

But something unexpected then began starting in early April – markets staged a recovery. The causes are up for debate, but probably have much to do with the fundamentally sound state of the US economy where unemployment was barely above 4%* and real wages are growing at well over 1% year-on-year*. Changes in the retail investing landscape have also been supportive, as a growing cohort of young investors engage in discussion forums like Reddit and trade on app-based platforms like Robinhood. Analysis by The Economist and Vanda Research has revealed a dip-buying instinct among this emerging class of US retail investors which was particularly pronounced in the aftermath of Liberation Day. Away from equities, the usually sedate world of bonds was rocked by the new US spending bill which was passed by the House of Representatives by a single vote in late May. Yields in 30-year bonds both in America and around the world rocketed upwards at the prospect of unsustainable increases in the US deficit which already measured a cool near-7% of total Gross Domestic Product (GDP) *. In the UK and Japan, higher-than-expected inflation further fuelled the move in their long-dated bonds while German yields rose for ‘good’ reasons, namely the expected increase in spending (and therefore growth) on infrastructure and the army. Again, the stockmarket was sanguine, even though higher bond yields normally imply a higher discount rate and therefore lower price for all assets, as well as a higher cost of capital for corporations.

As if all this wasn’t enough, a third and final test of the second quarter presented itself in the form of Israel’s (later joined by the US) attack on Iran’s nuclear infrastructure. The precedent for Israeli pre-emptive assaults on its enemies’ nuclear capabilities goes back to the 1981 Osirak reactor strike, so in a sense this wasn’t a surprise given the previous breakdown in negotiations with Iran. Nor was the initial reaction in markets in the form of a jump in oil prices, Japanese yen and Swiss franc, and of course falling equities. But then unexpected calm descended once again. Brent crude oil futures remained below USD 70* by the end of the quarter, compared with over USD 120* on Russia’s invasion of Ukraine. And stockmarkets were rallying again.

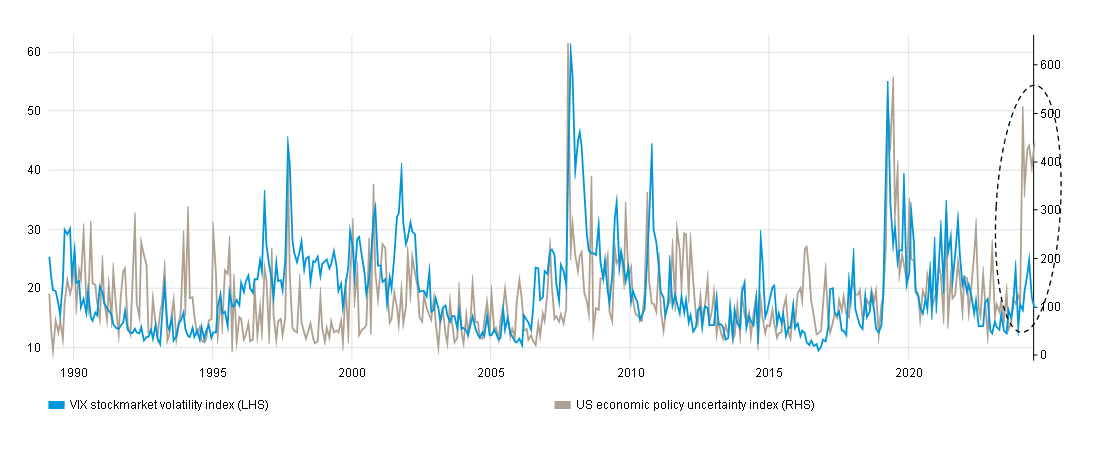

Chart 1: Unbelievably calm – markets just ignoring world events:

From 31 Jan 1990 to 30 June 2025

Source: Bloomberg, Policyuncertainty.com

Past performance is not an indicator of future performance and current or future trends.

Past performance is not an indicator of future performance and current or future trends.

Positioning

Portfolios will always be structurally positioned to capitalise on the superior real returns that stocks have historically offered over time, blended with carefully selected and sized diversifiers according to each multi-asset strategy's risk/return profile. The structural case for stocks remains undimmed in our view, hence we remain moderately engaged in equities. In regional equity terms, we favour marginally greater exposure to the US versus the MSCI AC World Index, with a similar stance to still-undervalued European equities and Japan. However, we are slightly cautious on emerging markets and China given the latter’s continuing economic challenges and the on-going geopolitical risks surrounding trade with the US and the Taiwan question.

Beyond stocks, our focus is inevitably on achieving effective diversification. Longer-dated government bonds as described above have become sources of unexpected risk in themselves as they attempt to price in both higher inflation from tariffs as well as a potential risk premium arising from extended government deficits. While our diversification strategy centres on fixed income and credit, we are wary of very long-dated bonds (which are most sensitive to changes in growth and inflation expectations), instead preferring a spread of different approaches and styles. For example, we favour short-dated bond and money market instruments which continue to offer compelling risk-adjusted yield characteristics, while we believe holdings in government bonds of around 10-year maturity are warranted for portfolio crash protection. Carefully screened investment grade corporate bonds - both short and medium-dated - play a role in generating sustainable yield too. In addition, we see a role for mortgage-backed, subordinated financial, climate and insurance-linked bonds for diversification purposes.

Finally, we believe that exposure to alternative investments can be more modest given the overwhelming need for absolute reliability away from equities, but candidates here could include long/short merger arbitrage, macro trading, real estate and gold, depending on specific investor aims. Gold has been a significant beneficiary of rising uncertainty this year so far, the continuation of a trend we have seen across successive crises since the Global Financial Crisis of 2008. The blend of asset classes described is, very simply, designed to deliver upside participation in the long-term gains the stockmarket tends to deliver, while smoothing out the volatility that many investors wish to avoid as they journey towards their long-term investment goals.

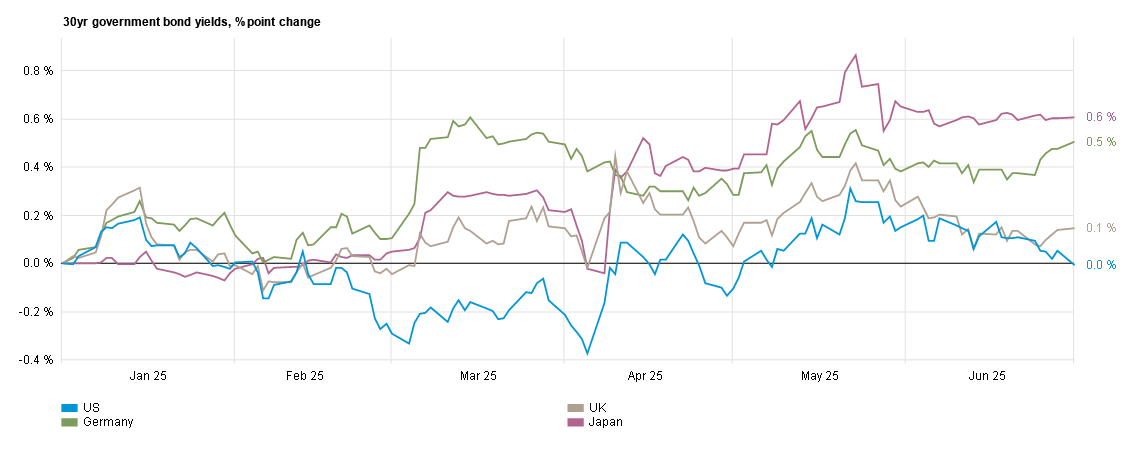

Chart 2: Diversification? Long-dated bond yields jumped in May:

From 31 Dec 2024 to 30 Jun 2025

Source: Bloomberg

Past performance is not an indicator of future performance and current or future trends.

Past performance is not an indicator of future performance and current or future trends.

Outlook

Normally any investment outlook anticipating geopolitical or political turbulence would be safe in its warnings that market upset will follow hot on its heels. While the former seems likely, the latter is now far less certain. The second quarter of the year followed a slightly unnerving pattern of presenting a series of extreme events without any enduring adverse stockmarket consequences. The question then becomes whether this will continue. The next few weeks and months are likely to see, inter alia, the culmination of the Israel-US-Iran conflict, negotiations over the Trump administration’s “Big, beautiful bill” before the Senate deadline of 4 July (which, in fact, passed by a single vote on 1 July), and on-going tussles over tariffs as various extensions and reprieves granted to America’s trading partners expire. And all this is before factoring in the unexpected which, as the year so far has shown, can come from anywhere and at any moment.

The fact that the US economy remains in good shape is encouraging and America is not about to lose its inherent competitive advantages, such as quality of management, technological prowess and energy self-sufficiency among others. But a sudden loss of investor patience with everything being thrown at them should not be completely discounted. The decline so far this year in the US dollar against most major currencies suggests a steady capital flight out of the world’s largest economy, while gold’s rise through each successive crisis speaks of deep lingering concerns around geopolitical risks which America itself appears to be contributing to. It is not inconceivable that even retail investors eventually tire of following the drama coming out of Washington and reassess their engagement in stockmarkets. Wall Street meanwhile continues to engineer new strategies designed to cope with this unpredictable new age with mixed results – see, for example, the fast-growing Equity Hedged ETF sector. But traditional multi-asset allocations consisting of equities and a mix of bonds have fared relatively well this year and can potentially continue to offer investors a risk-controlled pathway through the uncertainty.

Julian Howard is Chief Multi-Asset Investment Strategist at GAM Investments. This article represents the views of GAM’s Multi-Asset team.

*Source: Bloomberg, July 2025