Chinese stocks have far outpaced gains in global equities lately. Resilience in exports in the face of US tariffs and rate cuts may not tell the whole story. But a domestic cultural savings shift into stocks might.

30 September 2025

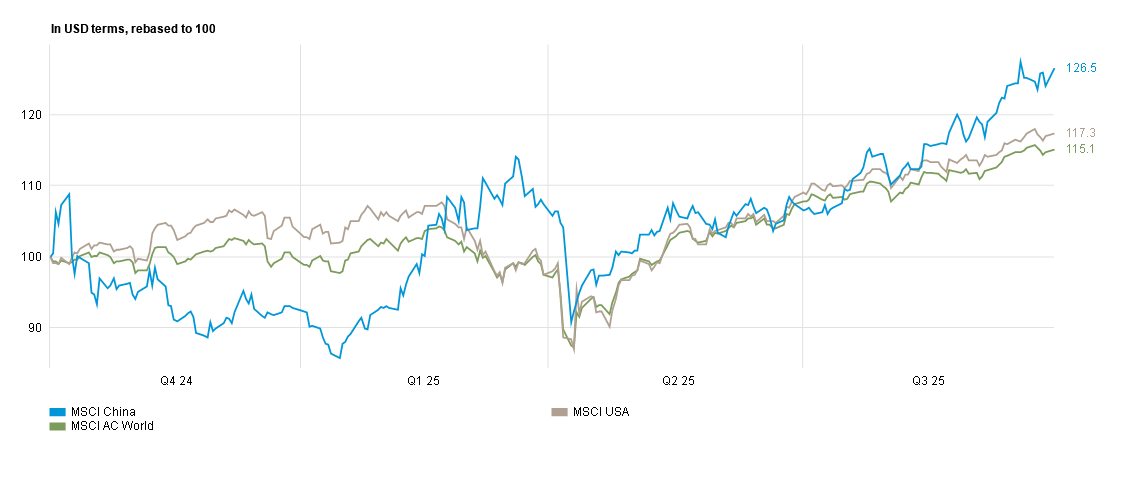

China’s stock market, as measured by the MSCI China Index in USD terms, is up nearly 27% over the last 12 months. On the same basis US stocks, as measured by the MSCI USA Index, and world stocks, as measured by the MSCI AC World index, are up ‘just’ 15% and 17% respectively. While news out of America is dominated by its chaotic politics, the underlying fundamentals of corporate earnings and consumption are in reasonable shape there. And of course America dominates the global equity index to the tune of 70%.

China, however, has arguably more profound challenges facing its economy and corporations. The first is one of overcapacity, particularly in areas such as electric vehicles (EVs) and solar panels. One recent report estimated that there were around 100 EV firms in China and, while few would doubt the quality and innovation of firms such as BYD, there can be such a thing as too much competition in a sector. The same issue plagues the solar panel industry. Simultaneously, Chinese retail sales appear sluggish as consumers continue to grapple with the fallout of a real estate crash.

What then, could explain the optimism implied in the stock market? Some point to China’s export resilience in the face of US tariffs, others to the government’s cutting of rates a year ago which allowed firms to buy back their own stock. The government’s ‘anti-involution’ campaign to reduce excess capacity in heavily subsidised industries may also be helping. But perhaps the most persuasive driver is the asset re-allocation that is starting to happen as consumers switch out of cash deposits into stocks. A genuine cultural savings shift into stocks would likely create a more sustainable return pathway for Chinese markets away from the boom-and-bust cycle that has characterised the last two decades. But any signs of a near-term speculative bubble could prompt a response. Premier Li Qiang has recently spoken of “orderly expansion” and “risk control mechanisms”, a clear hint that the authorities stand ready to intervene if things get out of hand. Be that as it may, the long-term case for Chinese equities remains clear – they represent just 3% of the MSCI AC World Index while the Chinese economy represents nearly 20% of the world’s in purchasing power parity terms.

From 30 Sep 2024 to 29 Sep 2025

Source: Bloomberg

Past performance is not an indicator of future performance and current or future trends.

Past performance is not an indicator of future performance and current or future trends.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not an indicator for the current or future development.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not an indicator for the current or future development.