Delivering on net zero commitments by 2050 will be very challenging, affecting every industry and requiring vastly more resources than many policymakers appreciate, or will admit to their electorates. But for investors, the ambitious drive towards decarbonisation is presenting compelling opportunities across a range of European companies.

06 June 2024

From the United Nations to the European Union, the commitment to hit net zero targets by 2050 has seemingly been set in stone.

In practice, beyond the sloganeering, achieving these hugely ambitious and very laudable targets will be much easier said than done. However, as managers of our clients’ savings, we believe that the decarbonisation drive represents a major opportunity to provide long-term returns for our investors.

For some time, the drive towards decarbonisation has presented a swathe of opportunities and we have sought to position our portfolios to capitalise on what we believe are the most compelling prospects for sustained, long-term earnings growth presented by the drive towards net zero.

How investors take advantage of the opportunities presented by the decarbonisation and the capex super cycle – alongside others shaping what we term the new era – from normalisation of interest rates, the rise of the Asian middle class and digital transformation, will define the long-term returns they can expect from their portfolio.

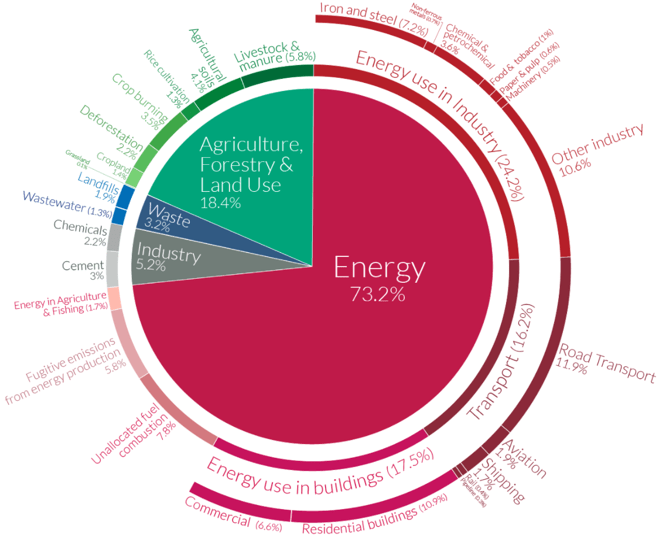

Hitting net zero by 2050: A daunting challenge

Source: Climate Watch, the World Resources Institute as at 2016.

The inconvenient truth is that energy demand will continue to rise; this demand growth will be driven by the increasing global population but more importantly by higher energy consumption per capita in emerging markets where energy consumption per capita is a fraction of developed markets’ levels. And unless supply rises to meet growing demand developing nations could continue to use the source most available to them – coal, or even wood in the least developed countries. Coal is not only bad for human health given resultant air pollution but also releases double the CO2 per unit of energy generated by gas. We believe energy/resource capex – particularly in gas, a key transition fuel and back-up for intermittent renewables – needs to pick up or the world will likely see higher prices for energy, and even shortages as well as higher coal consumption.

We must also consider the political challenges for leaders requiring their voters to reduce their carbon emissions – the cost of which is more immediately apparent than the longer-term environmental benefits. With some politicians already facing an element of voter pushback in their quest to implement net zero – while still standing a chance of being re-elected – we cannot rule out some further slippage in the realistic timescale. Admirable as the 2050 target may be, in the real world, for technological, financial and political reasons, it is deeply challenging. And we have left it far too late to act!

The new capital investment journey – from rust to boom?

According to the IEA1, to reach net zero emissions by 2050, annual clean energy investment worldwide will need to more than triple by 2030 to around USD 4 trillion.

With decarbonisation a key policy priority in the US and Europe, physical capex across the OECD will need to pick up very significantly. When it comes to the question of how existing infrastructure is set to handle the decarbonisation transition, the reality is that capex was too low for an extended period following the global financial crises, with infrastructure and capital stock across many developed countries both old and in poor shape.

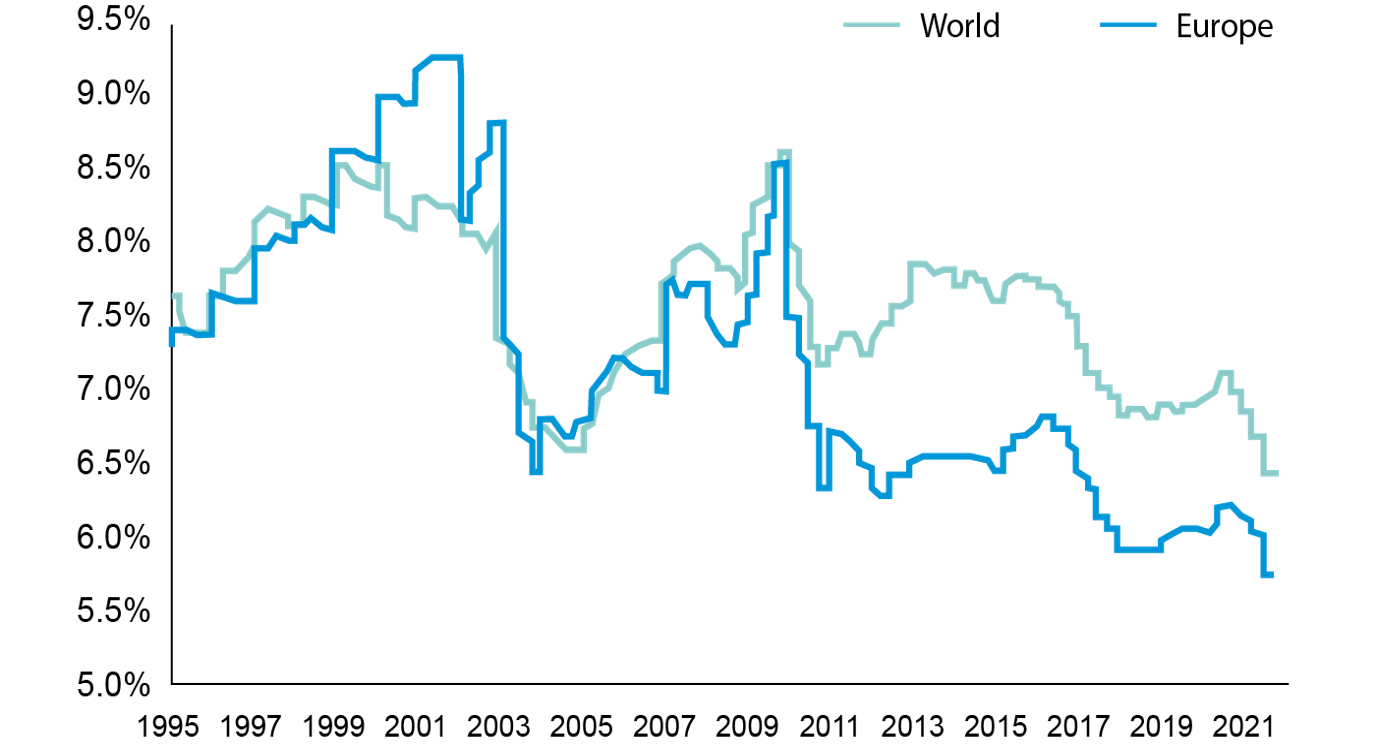

Corporate capital expenditure at low levels

Companies have reduced their CAPEX as a % of revenues since GFC

Source: DataStream, Goldman Sachs Global Investment Research data as at 30 Sep 2021. The views are that of the manager and are subject to change.

In the US, the Inflation Reduction Act and other measures amount to circa USD 2 trillion of direct or indirect funding. Europe needs to respond – both financially and in terms of planning reforms – or will continue to fall behind.

Facilitating the energy transition – and having any hope of approaching, let alone meeting, net zero targets by 2050 – will require a surge in capex across a range of sectors and industries ranging from the energy industry itself, electrification (well beyond vehicles), residential and commercial building refurbishment, and industrial & process industries.

Net zero is a huge opportunity to provide returns for our investors

As an investment management company, it is our role to deliver attractive returns for the people who trust us to manage their savings. We are focused on the opportunities presented by the decarbonisation theme. And such is the scale of policymakers’ ambition, and the difficulties they are only now coming to terms with in achieving it, the investment opportunities span a whole breadth of industries, each of which have a role to play.

Capturing opportunities within the energy system

We believe that many of the most compelling opportunities we see are within existing businesses closely associated with the energy systems we rely on today. While some net zero advocates might want to abandon, or urge the divestment of existing energy businesses entirely, in the real world we believe that the existing, large companies have a huge role to play if we are to make meaningful progress on decarbonisation. Globally, these companies – many of which, like Shell and Total, we have been favouring for an extended period within our European portfolios – have the expertise of thousands of highly skilled engineers and project managers as well as market positioning, deep knowledge of how the energy systems work and hundreds of billions of dollars of operating cash flow each year to support and drive the energy transition. These companies should not be marginalised by the energy transition – they need to be front and central to the future of low carbon energy if we wish to have any prospect of success in decarbonisation.

Within the energy system, the transmission and distribution of electricity is proving a significant bottleneck. Rising electricity demand (and the required complexity of the system) will necessitate refurbishments, strengthening and replacement of existing systems. Transmission and distribution grids will need to become many times larger - up to five-fold globally, according to some estimates. We believe companies like Prysmian, Schneider Electric, Linde and Atlas Copco – positions in our portfolios – are well-placed to play a key role in the expansion of power grids and the required surge in investment in the energy system.

Power grids

The biggest bottleneck?

Global power transmission lines need to rise 5x by 2050, from 7m to 35m circuit kilometres, as electricity demand rises 2.5x and transmission intensity rises by 2.25x

Past and current trends should not be relied upon as an indicator of future trends.

Source: Thunder Said Energy, March 2024

Source: Thunder Said Energy, March 2024

Another cost of decarbonisation of the energy system is the requirement for resiliency, energy storage and a source of backup power. Biofuels and synthetic fuels, which are often produced from renewable resources, can also play a role in reducing greenhouse gas emissions, with sustainable aviation fuel seen as a vital element of the airline industry’s commitment to meeting net zero goals. Meanwhile, green and blue hydrogen – which are respectively produced by electrolysing water using renewable energy and from natural gas using carbon capture and storage (CCS) – can be used as transport fuel, for industrial processes and as a form of energy storage. However, to date, many of these new technologies are still relying on government support, with costs far exceeding those offered by traditional technology. We are therefore wary to invest here outside of existing companies delivering attractive return on capital (ROC) such as Atlas Copco and Linde which can benefit by incrementally extending their product offerings in these segments. And natural gas, potentially with CCS, should have a large role to play in the back- up of intermittent renewable energy.

Building a lower-carbon future: construction, mobility and industrial processes

Modern building systems are continually evolving to support a greener future, driven by ever-changing consumer expectations and more environmentally friendly building requirements. This includes the construction of new buildings, and the refurbishment of existing assets. To capitalise on demand for low-carbon building solutions including insulation and the provision of rental equipment, companies like Kingspan, Saint Gobain and Ashtead are long-standing overweight holdings across our portfolios.

In mobility, transport infrastructure has a big role to play to achieve progress on climate-related goals. In the automotive value chain, we like companies such as Infineon and ST Micro that supply the power semi-conductors – a core part of electric vehicle powertrains. Looking beyond electric cars, companies we favour – such as truck maker Volvo - are helping to shape a more sustainable future in the electrification of buses, trucks and heavy construction equipment.

Finally, driven in part by regulatory developments, industrial processes are evolving to support a lower-carbon future. Traditionally emission-intensive manufacturing of basic products like cement, bricks and steel can become less environmentally damaging – albeit while passing on the higher costs to customers – through measures such as the use of biomass or waste-derived fuels, or through the use of CCS technologies. We have exposure to this through Linde and Atlas Copco, companies we believe offer attractive return potential.

Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

Investing in the energy transition is one of our key investment themes

Vital as Europe’s decarbonisation push is, we believe the true cost – and the scale of the investment opportunity – is only now becoming apparent to many. We believe that the companies we hold within our portfolios will be at the forefront of developments in the decarbonisation process. While we maintain our view that the timescale for achieving the net zero goal is challenging, the need to approach net zero is beyond debate and the investment opportunity represented by the decarbonisation path is, we believe, extraordinary, and we have long-since sought to position our portfolios to benefit from growing spending.

We believe decarbonisation and the capex super cycle will be key investment themes that can drive European equity performance.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

Equity: investments in equities (directly or indirectly via derivatives) may be subject to significant fluctuations in value.

Capital at Risk: All financial investments involve an element of risk. Therefore, the value of the investment and the income from it will vary and the initial investment amount cannot be guaranteed.

Concentration Risk: Concentration in a limited number of securities and industry sectors may result in more volatility than investing in broadly diversified funds.

Source: GAM, unless otherwise stated. GAM has not in¬dependently verified the information from other sources and GAM gives no assurance, expressed or implied, as to whether such information is accurate, true or complete. The information in this document is given for information purposes only and does not qualify as investment advice or as meeting any particular financial objectives, risk profiles, sustainability preferences or sustainability-related objectives of the recipient.

Specific links to third party websites are being provided for informational purposes only to reference the sources of certain information reflected herein and should not be construed that GAM is endorsing the content or views presented therein nor that GAM has independently verified such information or content.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

Equity: investments in equities (directly or indirectly via derivatives) may be subject to significant fluctuations in value.

Capital at Risk: All financial investments involve an element of risk. Therefore, the value of the investment and the income from it will vary and the initial investment amount cannot be guaranteed.

Concentration Risk: Concentration in a limited number of securities and industry sectors may result in more volatility than investing in broadly diversified funds.

Source: GAM, unless otherwise stated. GAM has not in¬dependently verified the information from other sources and GAM gives no assurance, expressed or implied, as to whether such information is accurate, true or complete. The information in this document is given for information purposes only and does not qualify as investment advice or as meeting any particular financial objectives, risk profiles, sustainability preferences or sustainability-related objectives of the recipient.

Specific links to third party websites are being provided for informational purposes only to reference the sources of certain information reflected herein and should not be construed that GAM is endorsing the content or views presented therein nor that GAM has independently verified such information or content.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.