‘Liberation Day’ and its aftermath have left investors shaken and bruised. Recognising that in the short term markets trade on sentiment is vital. During the present uncertainty, investors could do well to remember that equity buy-and-hold - with effective diversification - remains a well-proven approach.

30 April 2025

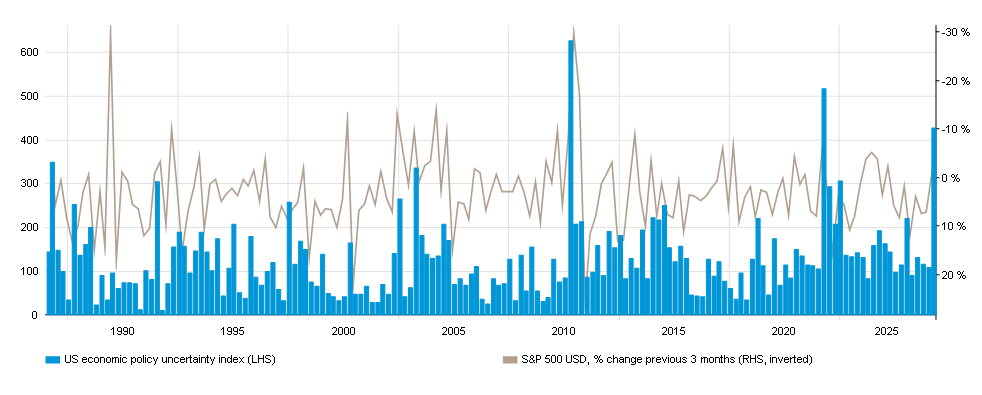

Historically, political developments have often created near-term ripples in financial markets, leading to uncertainty and unwanted volatility. By way of visual evidence, as shown below, the US policy uncertainty index has charted historical instances of the words ‘policy’ and ‘uncertainty’ across the media and – when overlaid with the S&P 500 Index – neatly reveals how much markets really, really do dislike uncertainty in the short term. For multi-asset investors, navigating the second Trump administration demands a disciplined approach and adherence to the fundamental investment principles set out when they first matched their investment goals to an asset allocation framework. For such a blended portfolio to work there needs to be a recognition that the superior returns offered by equities can only be predictably accessed over the long term, while excess volatility is best managed via a simple and transparent diversification strategy that actually delivers, and reliably so.

It's true – markets really hate uncertainty:

From 31 Jan 1985 to 31 Mar 2025

Source: Policyuncertainty.com, RIMES

Past performance is not an indicator of future performance and current or future trends.

Past performance is not an indicator of future performance and current or future trends.

Constantly do…very little

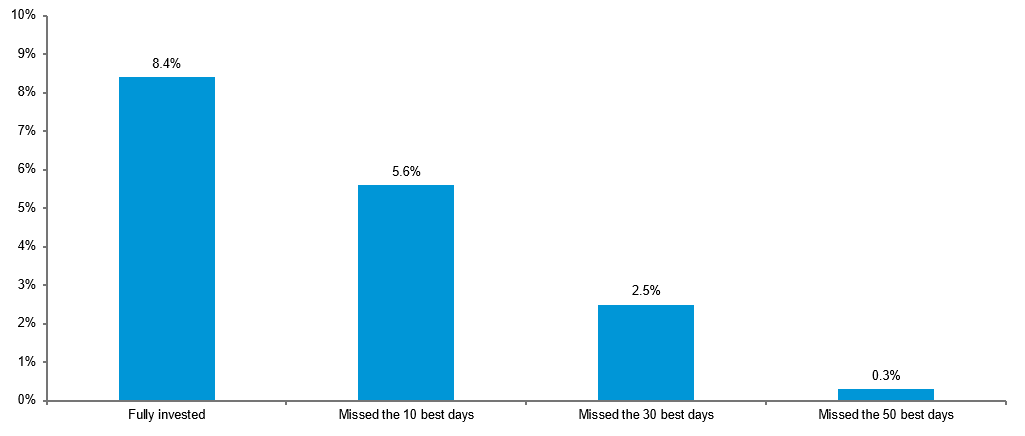

Stocks have historically delivered robust long-term returns, net of periods of volatility which have included coups, famines, pandemics, market crashes, depressions, financial crises and recessions. Professor Jeremy Siegel, author of buy-and-hold bible ‘Stocks for the long run’, has demonstrated that the US stock market over a multi-decade period has generated a real (after inflation) return of 6.5%-7%1 - the so-called Siegel Constant. The resilience and mean reversion demonstrated by the US stock market highlights the importance of staying invested and focusing on the bigger picture. Only by staying the course can investors benefit from the compounding effect of long-term growth. The issue is that short-term market movements are overwhelmingly tempting for investors seeking quick gains, and never more so than today given how technology like smartphones gives every investor access to live market data, day and night. And when it comes to the pursuit of quick and easy profits, listed stocks exhibit a unique contradiction in this regard. While the weight of academic evidence per above demonstrates that a long-term approach will yield favourable results, stocks themselves can of course be traded on a second-by-second basis (or even faster for algorithmic traders). For some, the temptation is just too much, but history has shown that reacting impulsively to political or indeed any other kind of event can lead to lower returns and excess volatility. Short-term trading can end up like chasing shadows - unpredictable and often driven by emotions and imagination rather than research-based logic. While near-term market events such as the imposition of trade tariffs can cause market fluctuations, investors who attempt to time these movements risk making decisions based on incomplete information or worse, fear, which can quickly erode their portfolio's value (see chart below).

The perils of being out of the market – even for a few days:

S&P 500 annualised returns from 31 Mar 1995 to 31 Mar 2025

Source: GAM

Past performance is not an indicator of future performance and current or future trends.

Past performance is not an indicator of future performance and current or future trends.

Stocks within the asset allocation context

To avoid succumbing to such temptations it is worth sticking to a set investment discipline. Sitting down with a professional advisor right at the outset to define investment objectives and the time horizon is vital since a clear pathway will help achieve the required focus. Virtually every multi-asset portfolio will contain an equity element to it since stocks have generally offered the best returns over time. But the size of this stock component must be carefully considered and then adhered to in order to maximise the chances of success.

Ang-st management – resisting market noise with disciplined portfolio rebalancing

As Dr. Andrew Ang, the well-known financial economist and author of over 100 publications, wrote back in 2012: “The foundation for a long-term investment strategy is rebalancing to fixed asset class positions which are determined in a one-period portfolio choice where the asset weights reflect the investor’s attitude toward risk.” In other words, investor suitability must be established and then the right asset allocation applied and stuck to religiously. If this is done correctly, market noise should not then prove a distraction since a blended portfolio will dampen stock volatility according to each investor’s risk tolerance anyway. Dr. Ang’s rebalancing point then comes into the equation and should represent the majority of on-going activity around a well-constructed investment portfolio. By regularly rebalancing to their target stock allocation, investors effectively buy low and sell high on a small-scale basis over time. For example, an equity allocation that has drifted below target usually reflects downward market movements and needs to be ‘topped up’ to stay on target (ie buying low, in effect), and vice versa when markets have rallied (selling high). Again, this minimises the temptation to opportunistically market time since portfolio trading is already part of an on-going routine.

Diversification – stable and predictable is best

Diversification is a cornerstone of investment strategy, with Harry Markowitz - widely regarded as the father of Modern Portfolio Theory - winning a Nobel prize for setting out the maths in the 1950s. The basic theory is that a diversified portfolio can offer less risk than a concentrated one without unduly sacrificing returns. While this all sounds clever – and it is – we do not need to be overly complex in the implementation. A simple and consistent approach to diversification can provide stability and reduce risk, especially during periods of negative sentiment such as markets are seeing today. In simple terms, diversification for the modern multi-asset portfolio involves spreading non-equity investments across asset classes and investment styles that behave independently of equities and which ideally just keep chugging along regardless of what is happening elsewhere. In this way, investors can protect their portfolios from the adverse effects of near-term volatility that impacts stocks.

The role of ‘sensible stalwarts’ as diversifiers

While the available universe of diversifiers is huge, a sensible and uncomplicated portfolio might hold just a handful of reliable stalwarts. These could include, inter alia, short-dated money market instruments, short-dated investment grade bonds issued by high quality companies, carefully selected climate bonds for risk-managed additional yield, gold for general risk aversion and inflation protection, and even standard long-dated government bonds for crash protection in extremis. Other diversification strategies are of course available but regardless, the aim should be for consistent return generation even if that return is generally lower than equities. Success here is defined by the diversifiers as a group strongly resisting any downturns incurred by stocks, whenever and however they may arise. If that has not been the case since February, it is probably time to review.

Noise cancelling for investors

Market volatility can result in sleepless nights and the last few weeks have been no exception. Technology and ever-faster dissemination of news keep us updated in ways unimaginable even 15 years ago, but we are left more frantic and wondering whether we should be acting on the cognitive flood. Will things get even worse? Or is now a good entry point? These are natural enough questions to ask amid the onslaught. Goal-based investing’s necessary response must be to ignore it all. And in many ways this approach provides blessed relief since the investment choices open to us each day are almost infinite and impossible to rationally assess. Instead, by staying true to their original asset allocations (assuming they remain suitable for their circumstances) by focusing on the long-term rate of return on stocks and maintaining a simple and consistent diversification strategy, investors are far more likely to achieve their long-term goals.

1University of Pennsylvania/Wharton School, 2006, https://magazine.wharton.upenn.edu/issues/summer-2006/the-next-long-run/

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The US Economic Policy Uncertainty Index is a measure of uncertainty related to economic policy in the US, developed by economists Scott Baker, Nicholas Bloom, and Steven J. Davis, using media coverage of policy-related uncertainties, Federal Tax code expirations and economic forecast differences as inputs.

The S&P 500 Index is a stock index tracking the performance of 500 of the largest, publicly traded companies in the US.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in indices which do not reflect the deduction of the investment manager’s fees or other trading expenses. Such indices are provided for illustrative purposes only. Indices are unmanaged and do not incur management fees, transaction costs or other expenses associated with an investment strategy. Therefore, comparisons to indices have limitations. There can be no assurance that a portfolio will match or outperform any particular index or benchmark.

This article contains forward-looking statements relating to the objectives, opportunities, and the future performance of the equity markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

This disclosure shall in no way constitute a waiver or limitation of any rights a person may have under such laws and/or regulations.

In the United Kingdom, this material has been issued and approved by GAM London Ltd, 8 Finsbury Circus, London EC2M 7GB, authorised and regulated by the Financial Conduct Authority.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The US Economic Policy Uncertainty Index is a measure of uncertainty related to economic policy in the US, developed by economists Scott Baker, Nicholas Bloom, and Steven J. Davis, using media coverage of policy-related uncertainties, Federal Tax code expirations and economic forecast differences as inputs.

The S&P 500 Index is a stock index tracking the performance of 500 of the largest, publicly traded companies in the US.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in indices which do not reflect the deduction of the investment manager’s fees or other trading expenses. Such indices are provided for illustrative purposes only. Indices are unmanaged and do not incur management fees, transaction costs or other expenses associated with an investment strategy. Therefore, comparisons to indices have limitations. There can be no assurance that a portfolio will match or outperform any particular index or benchmark.

This article contains forward-looking statements relating to the objectives, opportunities, and the future performance of the equity markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

This disclosure shall in no way constitute a waiver or limitation of any rights a person may have under such laws and/or regulations.

In the United Kingdom, this material has been issued and approved by GAM London Ltd, 8 Finsbury Circus, London EC2M 7GB, authorised and regulated by the Financial Conduct Authority.