With President Trump’s tax bill set to add trillions to US government debt and potentially fuel inflation, a bond buyers’ strike could test the ‘TACO’ theory ahead of the 4 July Senate vote.

04 June 2025

Something has been stirring in the otherwise sedate world of the 30-year global government bond market, with profound implications for investors.

In late May, a weak auction for US Treasuries precipitated a sharp sell-off not just in long-dated bonds but also stocks in the US and elsewhere. Stocks care about bond yields because they are effectively the discount rate by which the price of a series of future earnings streams - which is what stocks essentially are a claim to - is determined. Put simply, if yields go up stocks should, all other things being equal, go down. And the economy cares about bond yields because they influence mortgage rates and the cost of corporate borrowing. So the prospect of higher bond yields matters plenty for market participants.

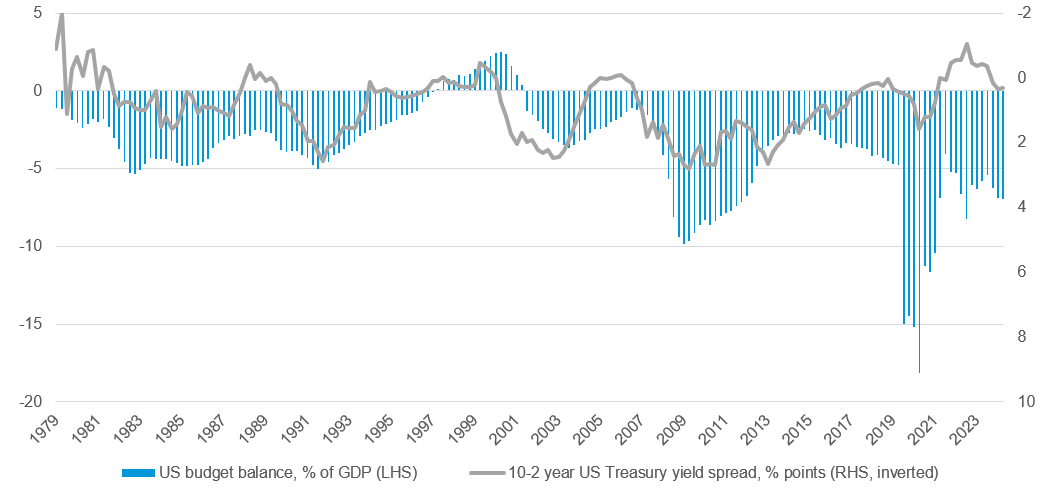

What has been driving them higher? The main cause has been the US government’s borrowing position. President Trump’s “Big, beautiful bill” was passed by the US House on the 22 May by a single vote before it passed to the Senate for approval. The tax bill will increase government debt by trillions of US dollars over the next decade and was arguably why the US lost its AAA credit rating recently. Even before the new bill gets passed, the US government has already borrowed around USD 2 trillion, or 6.9% of Gross Domestic Product (GDP) over the last year, while the Congressional Budget Office now sees that rising to 7.3% of GDP by 2050. By way of context, the average size of the deficit as a percentage of US GDP since 1980 has been just under 4%. The deficit today has never been so deep outside a recession, which makes it even more risky. With the US economy close to full capacity (see the low unemployment rate of 4.1%), more borrowing and stimulation of the economy now only adds to potential inflationary pressure. So a combination of both higher inflation and borrowing costs could be the result if the tax bill is passed by the Senate. While Republicans have argued that the resulting economic growth will generate more revenue, the bond market appears more sceptical. And herein lies a glimmer of hope. If the bond market really does go on strike as the cut-off date for the Senate passing the bill nears (4 July), it could yet result in said bill being dampened down. If nothing else, it will be a stern test of the TACO (Trump Always Chickens Out) theory currently doing the rounds. For investors whose nerves are still frayed by Liberation Day, it makes for an unenviable start to the summer season. Reliable diversification may be required.

Big, yes, but beauty is in the eye of the beholder:

Data from 31 Dec 1979 to 31 Mar 2025

Source: Bloomberg

Past performance is not an indicator of future performance and current or future trends.

Past performance is not an indicator of future performance and current or future trends.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not an indicator for the current or future development.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not an indicator for the current or future development.