President Trump’s short-lived threat to oust Chair Jerome Powell briefly roiled markets. Despite the Big, Beautiful Bill and sticky inflation, markets are already pricing in multiple rate cuts, even with no change to the Fed hot seat. And the bond markets vigilantes will be watching, whether Jay walks or not.

22 July 2025

Last week President Trump appeared to threaten to fire Federal Reserve (Fed) Chair Jerome Powell, and the market reaction was instructive. The S&P 500, the US dollar and longer-dated Treasuries all fell but the move was not especially pronounced and was starting to reverse even ahead of the President stating belatedly an hour later that “We’re not planning on doing anything.” This was important because it revealed in the minds of some commentators that the TACO (Trump Always Chickens Out) concept remained intact, and that the President generally sought to avoid stiff resistance or potential humiliation.

A Powell exit may not change the Fed’s tune

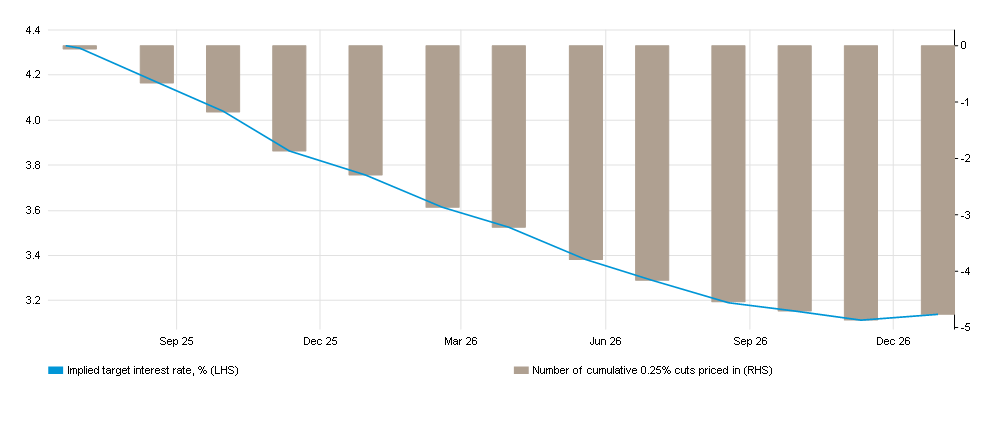

The perpetual delays and reprieves following his tariff threats appear to support this theory but the idea starts to look shaky when one considers the passing of the Big Beautiful Bill on 4 July which will inevitably expand the budget deficit to the dismay of much of his base (Elon included). Perhaps the market’s quick recovery suggested less that the President would not carry out his threat and more that any new Fed chair would not be so different from Jerome Powell. This may sound odd given the assumption that some kind of stooge would replace Powell at the Fed and immediately ease monetary policy. But futures markets today are suggesting that even under the current Powell regime, the Fed would cut rates five times (at 0.25% each) between now and January 2027, ie fully 1.25% to just over 3%. And Chair Powell himself has said that he wouldn’t rule out a first cut at the 29-30 July meeting. This may not be enough for the President, but for the markets the difference in the future rate trajectory between the incumbent and any (presumably dovish) replacement might really not be that wide after all.

Beware of the bond market vigilantes

Then there is of course the long-dated Treasury market itself which can and does impose discipline if required. Should rates be cut too far and too quickly even as inflation rises (it sits awkwardly at 2.7% and tariffs haven’t made themselves fully felt yet), those long-dated Treasury yields would likely jump in protest as they look to price in potentially uncontrolled inflation. Higher bond yields in turn threaten economic activity and would almost certainly force the administration (and by then the Fed too) to climb back down. The real danger however, would be if both the administration and any new Fed chair in a pique of frustration decide to completely ignore inflation and the bond market in a deliberate move to disprove the TACO adherents. The previous administration arguably lost the election because of inflation, so it would be ironic if the new one wilfully chose to ignore it in order to prove a point. So much for a quiet summer.

Futures market sees rate cuts even under Chair Powell’s leadership:

From 21 Jul 2025 to 27 Jan 2027

Past performance is not an indicator of future performance and current or future trends.

Source: Bloomberg

The views are those of the manager and are subject to change. For illustrative purposes only.

Source: Bloomberg

The views are those of the manager and are subject to change. For illustrative purposes only.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not an indicator for the current or future development.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not an indicator for the current or future development.