With US inflation lingering above target, tariff uncertainty persisting and major retailers warning of looming price hikes, the risk of consumer belt-tightening is real. As uncertainties abound, the case for effective diversification in multi-asset portfolios grows ever stronger.

21 May 2025

A question we are frequently asked is, “What is happening with inflation and also how is this affecting markets and your investment approach?”

Academic research reveals that predicting inflation consistently and accurately is a daunting task. Amid talk of inflation stabilisation today we still see several upside risks. In the US, it’s true that headline consumer price index (CPI) inflation has come off its 9.1% peak of nearly three years ago but it remains at 2.3% today (above the Federal Reserve-mandated target of 2%) and the data has not yet taken into account the anticipated inflation stemming from the Liberation Day tariffs and their associated disruption. While a 90-day tariff reprieve has been granted, retailers such as Walmart have warned that customers are likely to start seeing a more significant price impact in stores due to tariffs in the coming weeks.

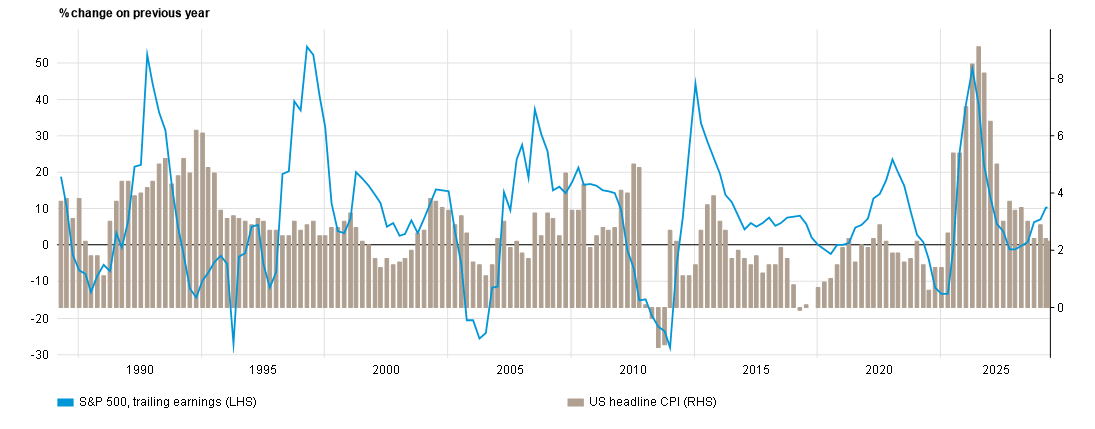

As for the market implications, we would note that over the medium-to-long term stocks have historically served as one of the best hedges against inflation, and during 2022 when inflation spiked on the back of post-pandemic supply chain disruption and energy prices rose following the invasion of Ukraine, US firms were on the whole able to pass prices on. So the fact that Walmart today is confident enough to warn its customers that price rises are coming speaks once again to the ability of corporate America to pass on cost push inflation and preserve margins.

It’s worth bearing in mind though that US stocks could yet struggle if consumers cut back their spending meaningfully. The housing market is a particular bellwether in this regard. If inflation does spike from here, 10-year US Treasury yields will correspondingly drive up yields on the all-important 30-year fixed mortgage rate. For American consumers the ability to “refi” at low rates is key to on-going confidence and house moves. 30-year fixed rate mortgages never really came down from the jump in yields seen in 2022 and are currently hovering at 6.9%, so any further increases could be detrimental.

What does all this mean for portfolios? Well, we do hold some longer-dated government bonds for diversification and crash protection in but we are not committed to a big directional view given the above. While we note that yields are relatively elevated compared with recent history at 4.5%, the enormous uncertainty around the future course of inflation gives us pause around any tactical positioning in this asset class. The key lesson here is that beyond equities, diversification should generally aim to minimise directional bets and focus on steady and reliable sources of return, for example short-dated T-Bills, high-quality investment grade, insurance-linked catastrophe bonds and alternative investments, such as macro investing by specialist traders. All are united by their low correlation to stocks and long-dated government bonds. If inflation does push traditional fixed income yields higher from here, these investments should act independently.

Stocks should act as a shield against inflation over time:

From 31 Mar 1985 to 30 Apr 2025

Source: Bloomberg

Indices cannot be purchased and invested in directly. Please refer to Appendix for full explanation of indices shown.

Past performance is not an indicator of future performance and current or future trends.

Indices cannot be purchased and invested in directly. Please refer to Appendix for full explanation of indices shown.

Past performance is not an indicator of future performance and current or future trends.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not an indicator for the current or future development.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not an indicator for the current or future development.