Der Versuch der Trump-Regierung, die globale Handelsordnung zu erschüttern, löste eine extreme Volatilität an den globalen Märkten aus. Während komprimierte Kreditspreads nur begrenztes Potenzial für attraktive Renditen zu bieten scheinen, erläutert Tom Mansley seine Ansicht, dass ein „Sweet Spot“ bei reifen hypothekenbesicherten Vermögenswerten in den USA eine überzeugende Anlagechance für Anleger darstellt.

11. Juli 2025

Politische Unsicherheit flankiert volatilen Start von Trump 2.0

Der unkonventionelle politische Ansatz der Trump-Regierung – von der Einführung weitreichender Handelszölle bis hin zu tiefgreifenden Kürzungen im Staatshaushalt und Plänen für umfangreiche Steuersenkungen für Unternehmen und Deregulierung – hat für beispiellose Unsicherheit unter Anlegern gesorgt.

Die Verluste nach dem „Liberation Day“ am 2. April sind zwar wieder ausgeglichen, aber dennoch ist die ganze Episode nicht ohne finanzielle Folgen geblieben.

Die Renditen von US-Staatsanleihen sind gestiegen, der US-Dollar ist eingebrochen, und Gold, ein traditioneller sicherer Hafen in Zeiten der Unsicherheit, ist in die Höhe geschnellt. Das wirft die Frage auf, ob die US-Währung überhaupt noch als „sicherer Hafen“ attraktiv ist.

US-Wohnungswirtschaft von Trumps Zöllen verschont geblieben

Während die Unsicherheit über die US-Handels- und Einwanderungspolitik sowie das vorgeschlagene Haushaltsgesetz, das die Staatsverschuldung erheblich erhöhen könnte, US-Staatsanleihen und den US-Dollar belastete, hatte das politische Hin und Her kaum Einfluss auf die inländischen Verbraucher und die Wohnungswirtschaft. Unserer Ansicht nach werden RMBS, also hypothekenbesicherte Wertpapiere, die durch Wohnimmobilien besichert sind, als vergleichsweise sicherer Hafen von Anlegern nach wie vor unterschätzt, trotz der hohen Spreads sowohl in der Vergangenheit als auch im Vergleich zu Anlageklassen wie Hochzinsanleihen.

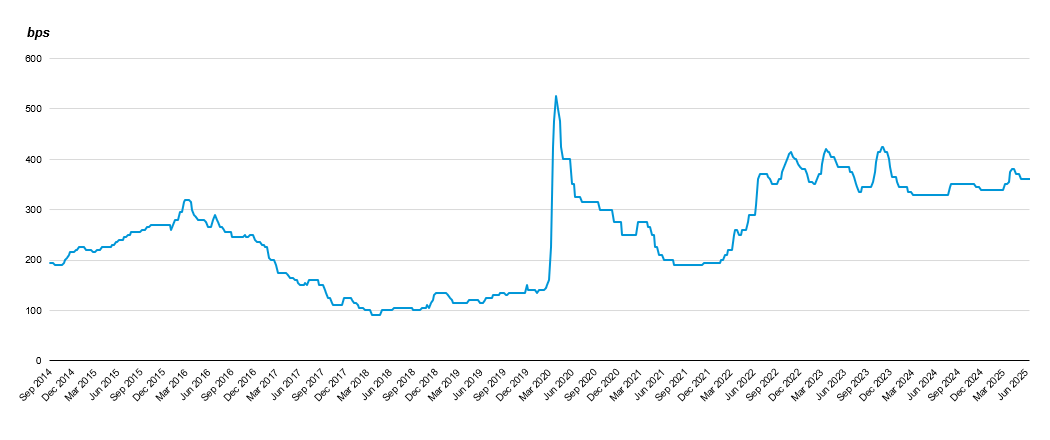

Historische Spreads von RMBS

Non-Agency

Vergangene und aktuelle Trends sollten nicht als Indikator für zukünftige Trends herangezogen werden.

Quelle: TRACE, Wells Fargo Securities, 20. Juni 2025. Chart wird vierteljährlich aktualisiert. Nur zur Veranschaulichung.

Quelle: TRACE, Wells Fargo Securities, 20. Juni 2025. Chart wird vierteljährlich aktualisiert. Nur zur Veranschaulichung.

Sicher wie Häuser? Warum wir die Aussichten für den US-Wohnimmobiliensektor positiv einschätzen

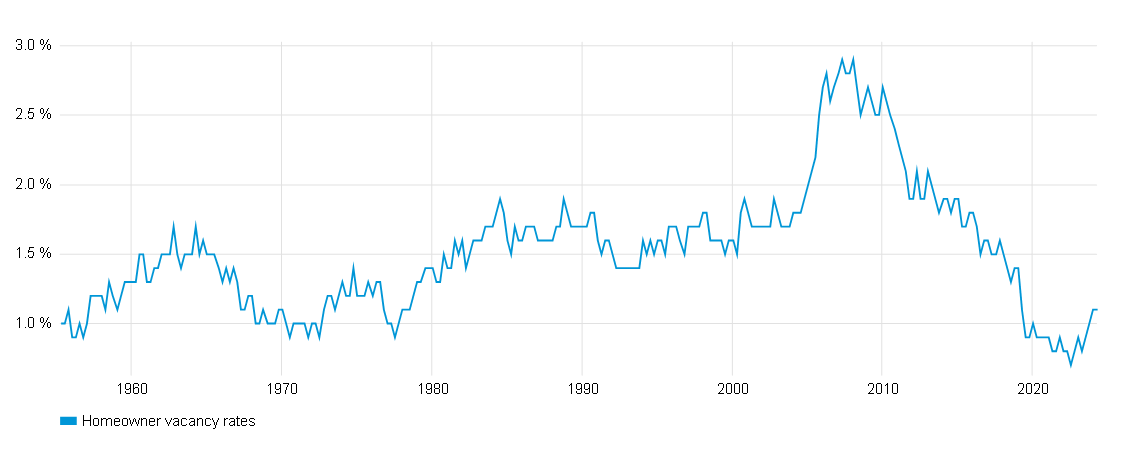

Trotz der Volatilität an den breiteren Anleihen- und Aktienmärkten sind wir der Ansicht, dass der Wohnimmobilienmarkt von relativer Konsistenz und zugrunde liegender Stärke geprägt ist. Aufgrund der stetigen Nachfrage von Käufern, des geringen Angebots und der positiven Kreditvergabemuster ist das vorrangige Thema, das wir mit Wohnimmobilien verbinden, die Stabilität. Angesichts des positiven wirtschaftlichen Umfelds liegen die Leerstandsquoten bei Eigenheimen mit rund einem Prozent in der Nähe ihrer historischen Tiefstände von vor einigen Jahrzehnten.

Leerstandsquoten bei Eigenheimen in den USA

31. März 1956 bis 31. März 2025

Die Wertentwicklung in der Vergangenheit ist kein Hinweis für die zukünftige Wertentwicklung bzw. aktuelle oder zukünftige Trends.

Quelle: Bloomberg.

Quelle: Bloomberg.

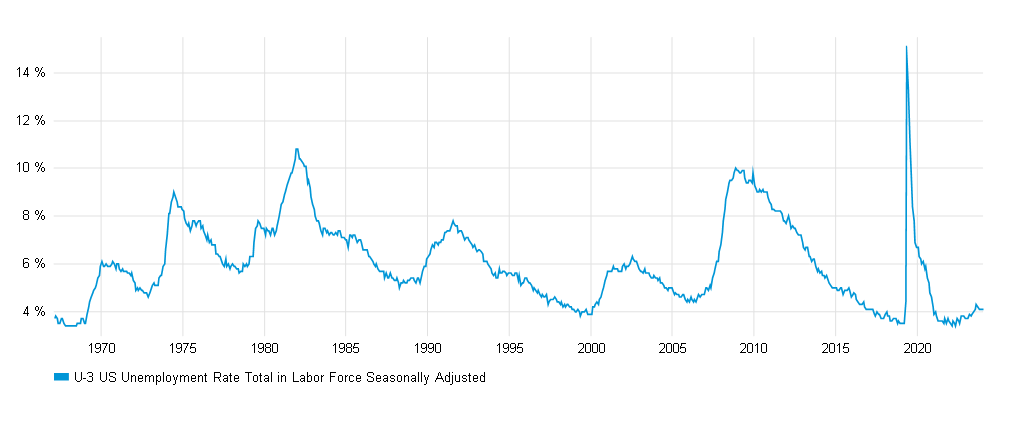

Gestützt durch die Widerstandsfähigkeit des Arbeitsmarktes – die sich in niedriger Arbeitslosigkeit und steigenden Löhnen manifestiert – sind die Ausfallraten und die Zahl der Zwangsvollstreckungen nach wie vor extrem niedrig, was die robuste Bonität der Kreditnehmer widerspiegelt und zeigt, dass die Rückzahlung ihres Hypothekendarlehens für sie Priorität hat.

Arbeitslosenquote in den USA

31. Januar 1968 bis 31. Dezember 2024

Quelle: Bloomberg.

Der „Sweetest Spot“ im riesigen Universum hypothekenbesicherter US-Wertpapiere

Die schiere Grösse des Universums hypothekenbesicherter Wertpapiere mag einige Anleger überraschen – es handelt sich um einen hochliquiden, diversifizierten Markt mit einem Volumen von über 10,8 Bio. USD1, auf den etwa ein Viertel des gesamten US-Anleihenuniversums entfällt. Als sehr grosses Segment des US-Anleihenmarkts bietet der RMBS-Bereich aktiven Managern enorme Chancen, weil die Auswahl riesig ist.

Während einige Anleger Agency-Kredite bevorzugen, konzentrieren wir uns auf Kernpositionen schon viele Jahre laufender Hypotheken auf Wohnimmobilien, insbesondere solche, die im Zeitraum 2004-2008 vergeben wurden. Unserer Meinung nach machen mehrere Faktoren diese Anlagen besonders attraktiv:

- Hoher Basiswert im Verhältnis zum Kreditumfang: Diese Vintage-Hypotheken wurden vergeben, als die Eigenheimpreise deutlich niedriger waren als heute, d. h., die Kreditnehmer haben sich mit ihren Immobilien im Laufe der Zeit erhebliches Eigenkapital aufgebaut. Somit profitieren Anleger in diesen Anlagewerten als abgesicherte Kreditgeber von einem niedrigen Beleihungsauslauf (Verhältnis des Kreditbetrags zum Verkehrs- oder Marktwert einer Immobilie).

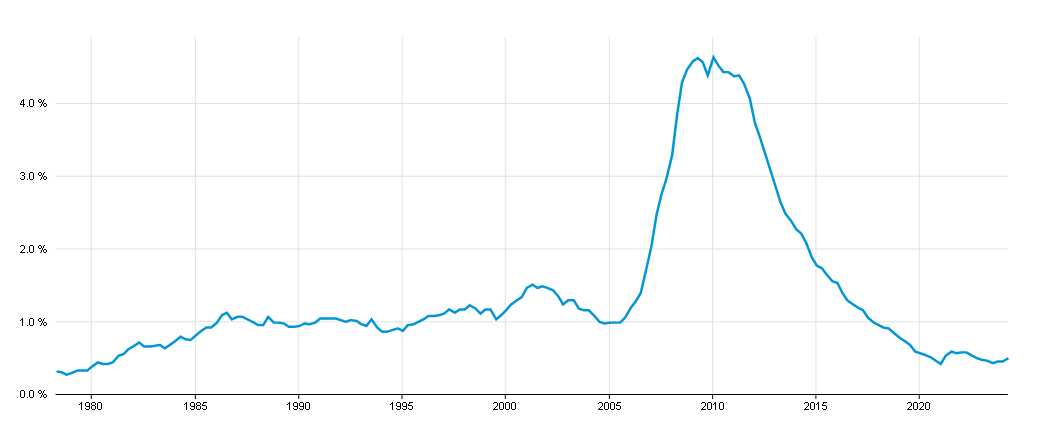

- Langjährige Hypothekengläubiger weisen eine stabile Tilgungshistorie auf: Unserer Ansicht nach entstand das höchste Ausfallrisiko bei Hypotheken rund um den „Sweet Spot“ von 2005 nach der globalen Finanzkrise der Jahre 2007-2008. Seitdem sind die Zwangsvollstreckungsraten sogar unter den Ausgangswert von 1990 bis 2005 gesunken, was darauf hindeutet, dass Hypothekengläubiger ihre Schulden in guten wie auch in schlechten Zeiten bedient haben und gleichzeitig vom stetigen Anstieg der Immobilienwerte profitierten.

Zwangsversteigerungen in % der Gesamtkredite (nicht saisonbereinigt)

31. März 1979 bis 31. März 2025

Die Wertentwicklung in der Vergangenheit ist kein Hinweis für die zukünftige Wertentwicklung bzw. aktuelle oder zukünftige Trends.

Die Wertentwicklung in der Vergangenheit ist kein Hinweis für die zukünftige Wertentwicklung bzw. aktuelle oder zukünftige Trends.

Quelle: Bloomberg. - Kreditnehmer zeigen geringe Sensitivität gegenüber Zinsschwankungen: Kreditnehmer, die in den Jahren 2004-2008 Hypotheken aufgenommen haben, die noch nicht getilgt sind, widerstanden jeder Versuchung, sich zu refinanzieren, selbst als die Zinssätze auf drei Prozent sanken. Da die Refinanzierungssätze inzwischen bei fast sieben Prozent liegen2, werden diese Kreditnehmer ihre Kredite jetzt wohl kaum vorzeitig zurückzahlen. Stattdessen werden sie weiterhin ihre regelmässigen Zahlungen leisten. Da viele ältere Hypotheken nun Diskontanleihen sind (d. h. unter dem Nennwert gehandelt werden), würden RMBS-Anleger auch dann, wenn die Hypothekengläubiger ihre Hypothek doch vorzeitig tilgen sollten, ihr Kapital im Wesentlichen rasch von einer Diskontanleihe zurückerhalten, die sich schneller dem Nennwert nähert – dadurch erhöht sich auch ihre Rendite. Somit unterstützen Kreditnehmer, die sich für eine schnellere Rückzahlung entscheiden, das Ertragselement der Gesamtrendite, die Anleger aus RMBS-Portfolios erhalten.

Absicherung des Zinsänderungsrisikos, um eine Prämie zu erzielen

Der Besitz eines Kernportfolios aus älteren, stabilen Hypotheken, insbesondere eines solchen, das auf Kreditnehmer ausgerichtet ist, die während der gesamten Laufzeit Rückzahlungen leisten, dürfte unserer Ansicht nach dazu beitragen, das Risiko einer vorzeitigen Tilgung zu reduzieren und dadurch die Duration vorhersehbarer zu machen. Das Zinsrisiko bleibt zwar bestehen, kann jedoch leicht durch den Einsatz von Treasury-Bond-Futures gemindert werden, mit denen wir das Zinsrisiko des Portfolios reduzieren und die Volatilität weiter senken. Auf diese Weise kann ein Portfolio nach unserer Einschätzung die Erträge von Hochzinsanleihen nachbilden, gleichzeitig ist die Korrelation zu anderen Anlageklassen gering.

RMBS – gestützt auf ein starkes Fundament

Während sich Schockwellen durch globale Ereignisse wie dem Scheitern des Long Term Capital Management Hedgefonds im Jahr 1998, der Finanzkrise von 2007/2008 und der Covid-Pandemie auf praktisch jede Anlageklasse auswirken können, sind wir der Ansicht, dass der US-Hypothekenanleihenmarkt heute besser geschützt ist denn je – dank einer Reihe unterstützender binnenwirtschaftlicher Faktoren wie einer anhaltend hohen Nachfrage nach Eigenheimen und einem robusten Arbeitsmarkt. Ungeachtet der Unsicherheiten in Verbindung mit dem politischen Kurs der US-Regierung, was nicht ohne Folgen für viele risikobehaftete Anlagen bleibt – insbesondere das exportabhängige verarbeitende Gewerbe sowie den Energie- und Pharmasektor – sind wir der Ansicht, dass Bereiche wie Wohnimmobilien und Verbraucherkredite von der politischen Agenda der Regierung verschont bleiben. Das Risiko ungünstiger gesetzlicher Entwicklungen wird dadurch verringert.

Im aktuellen Umfeld, das von politischer Unsicherheit geprägt ist, dürften RMBS-Portfolios, insbesondere solche, die sich auf ältere Hypotheken konzentrieren, weiterhin attraktive Renditen für Anleger erzielen. In einem volatilen Anlageumfeld könnten diese Renditen unserer Ansicht nach noch attraktiver sein. Obwohl diese Anleihen, die aus den Jahren 2004-2008 stammen, naturgemäss (Hypotheken sind befristet) nicht ewig verfügbar sein werden, sind wir der Meinung, dass dies ein ausgezeichneter Einstiegspunkt für den Kauf solcher Anlagewerte ist, die für Anleger in den kommenden Jahren weiterhin ein höchst attraktives Risiko-Rendite-Verhältnis bieten dürften.

Natürlich werden sich im riesigen RMBS-Universum im Laufe der Zeit andere ebenso attraktive Chancen ergeben, doch täten die Anleger unserer Einschätzung nach gut daran, von diesen unterschätzten Anlagewerten zu profitieren, solange sie noch verfügbar sind.

Tom Mansley leitet die Strategie für Mortgage-Backed Securities bei GAM Investments.

Quellen:

1Securities Industry and Financial Markets Association (SIFMA), Dezember 2021.

2Bloomberg, Juli 2025.

1Securities Industry and Financial Markets Association (SIFMA), Dezember 2021.

2Bloomberg, Juli 2025.