Amid the noise and chaos of tariffs and conflict in the Middle East, it is easy to forget about the humble Federal Reserve (Fed) whose job is to ‘just’ set the benchmark interest rate, which helps to price all assets.

25 June 2025

The Fed has of course been facing a policy dilemma for some time thanks in part to its often contradictory dual mandate of promoting full employment while simultaneously keeping inflation under 2%. Right now, unemployment is just over 4% and headline CPI inflation just over 2%, so not a bad scorecard. But the US economy has faced a series of shocks this year which have brought this into sharp relief, including the imposition of tariffs on imported goods as well as higher market-based interest rates due to an expansionary spending bill that is due to be approved by 4 July, and now conflict in the Middle East.

All of these threaten consumer confidence and therefore the economy, primarily through the channel of higher inflation. To its credit, the Fed has been open about the difficulties of choosing the next policy steps despite President Trump's colourful exhortations to cut rates regardless. Fed Chair Powell said on Tuesday that slightly softer economic data would have justified lower interest rates if it wasn't for concerns that tariffs would later push inflation upwards, as many of America's largest retailers such as Walmart and Target have been warning already.

In this sense, doing nothing appears to be a perfectly legitimate option until there is some more clarity, and his answers during Tuesday's congressional hearings hinted that it would be at least until the Fed's September meeting before any action on rates is taken. Fed-watching and the policy trade-offs described used to dominate financial headlines, particularly during times of geopolitical crisis, but stock markets appear sanguine to the point of indifference. Perhaps this is because the US economy remains in fundamentally reasonable shape. Either way, it will be worth monitoring whether elevated inflation expectations and depressed confidence start leaking faster into the real economy. Then all eyes will be back on the Fed and that pesky trade-off.

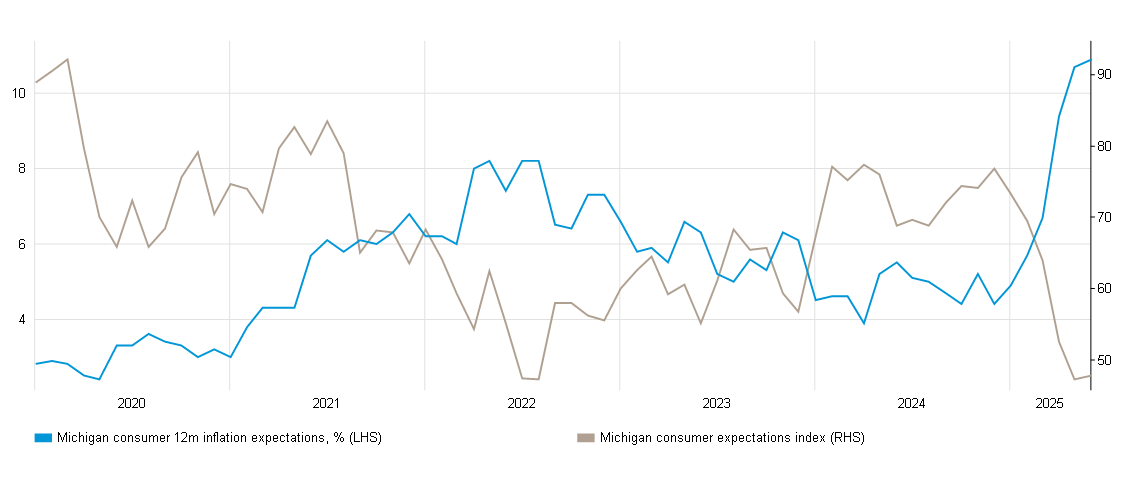

Self-fulfilling extremes in consumer sentiment and inflation expectations could yet force the Fed’s hand:

From 31 Dec 2019 to 31 May 2025

Source: Bloomberg, as at 31 May 2025.

Past performance is not an indicator of future performance and current or future trends.

Past performance is not an indicator of future performance and current or future trends.

Julian Howard is Chief Multi-Asset Investment Strategist at GAM Investments. This blog represents the views of GAM’s Multi-Asset team.

Important legal informationThe information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not an indicator for the current or future development.